By Richard A. Ciccarone, President & CEO of Merritt Research Services, LLC and Co-Owner of MUNINET, LLC

The Top 21% of Cities With High Pension Funding Levels Deserve Attention and Usually Praise

With so much well-deserved negative attention focused on cities with huge unfunded pension overhangs, it’s probably a good time to draw attention to the cities that are not burdened by pension liabilities. Cities, which maintain adequate pension set-aside contributions based on reasonable actuarial assumptions, usually fit the bill of practicing responsible management and earn a pat on the back.

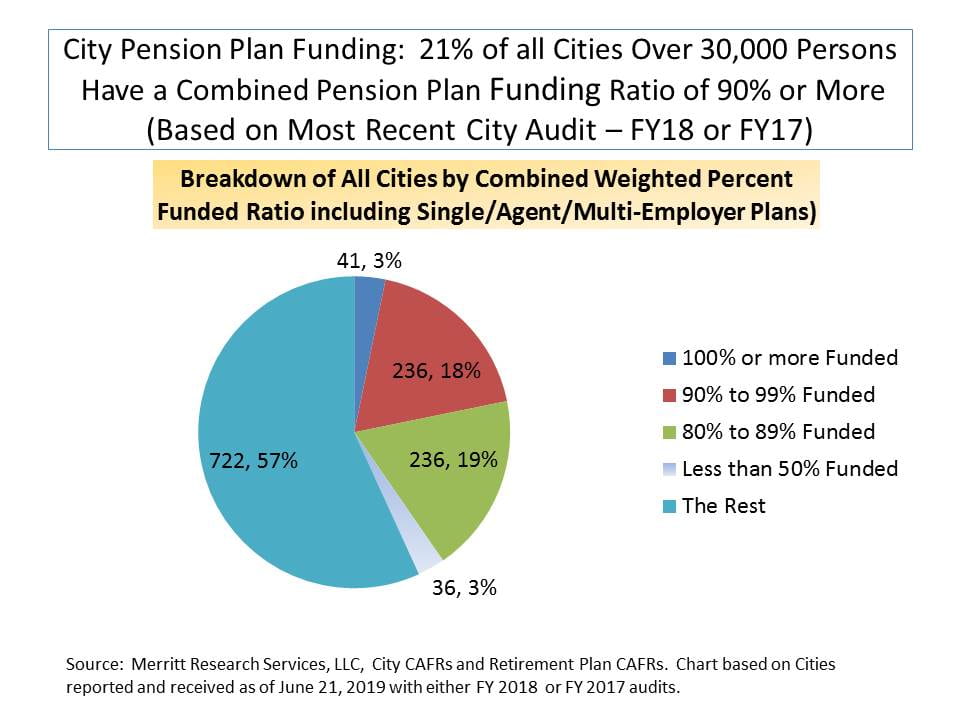

Only about three percent (3%) of all cities with populations of at least 30,000 have fully funded their total pension liabilities. Some of these have even overfunded their plans. Another 18% of these cities have funded their pension liabilities in the 90% to 99% range. That means that approximately 21% of all cities are in very good to excellent shape on pensions.

Beyond the best funded cities, 19% of all cities bear a marginally fair to good funding ratio of 80% to 89%.

In contrast to the top group of cities which have fully funded pensions, the pie chart below shows that an equal 3% of cities have consolidated pension plan funding ratios of less than 50%. By all measures, those plans are the most challenged and face the potential of eventual insolvency if the worst-case scenarios play out.

The remainder of all cities in the study carry a funding ratio between 50% and 80%.

This assessment of pension funding status is based on a new study of 1271 cities by Merritt Research Services, LLC, an independent municipal bond data and research company.

Chart 1. Percent Consolidated Funding Ratio Breakdown

The Merritt Research city funding ratio is calculated by deriving a consolidated funding position for each city by accounting for all of a city’s pension plans, regardless of whether they are the sole responsibility of that city (single or agent plans) or if they are a participant in a multiple employer plan, usually sponsored by the state.

All of the funding percentages are preliminary and likely to change somewhat since the analysis is based on the most recent city audits available to Merritt Research as of June 21, 2019. At the time of this study, 57% of the city audits included as the most recent end of year reports in the study related to fiscal year 2018 and the remainder applied to Fiscal Year 2017. As the new audits become available, the pension funding medians will adjust accordingly.

Because most city government audits take six months to a year, or longer, to be completed and reported, a large number of cities with fiscal years closing on December 31, 2018 are just becoming available.

To make matters more complicated, but without impacting the final analysis materially, city audit fiscal year end periods may differ from their individual pension plan audits. In those cases, the pension funding measurement period may lag the city audit fiscal year end by one year.

Which Cities Are The Best Funded?

The table below lists the top 25 funded pension plans in the United States for cities with populations over 30,000 based on the most recent fiscal year audit available.

At the top of the list is the city of Bristol, Connecticut with a substantial 2018 fiscal year end funded ratio of 148.2% Although an optimistic discount rate used by a plan could cause the funding ratio to be higher than would be typically expected, Bristol’s Merritt derived weighted average discount rate of 7.3% on its total pension liability falls close to middle of the pack among city pension plans nationally.

Following Bristol on the best funded pensions list are three cities in Michigan (Kalamazoo, Pontiac, and Troy), one in Missouri (Blue Springs), one in the state of Washington (Lakewood), and one in California (Fresno). Of those mentioned, Troy is the only one with a median household income that is significantly higher than the national average.

Pontiac may be a surprise city on the best funded list because it has been subject in recent years to the State of Michigan Treasury office’s financial emergency supervision program. Fresno, California, the largest city with an overfunded pension position, had its pension funding status substantially enhanced when it issued a large pension funding bond issue in 2002. Issuing pension bonds to pay down pension liabilities normally transfers risk to bondholders in place of pension plan beneficiaries.

Table 1. Top 25 Highest Funded U.S. Cities Based on Combined Pension Funding Ratio and Average Discount Rate on Combined Plans:

| City Name |

State | FY Used |

Population | Grand Total Funded Ratio % |

Derived Weighted Average Discount Rate on Total Pension Liability |

|

| Bristol | CT | 2018 | 60,110 | 148.22 | 7.30 | |

| Kalamazoo | MI | 2017 | 75,809 | 145.54 | 7.50 | |

| Pontiac | MI | 2018 | 60,053 | 143.59 | 7.24 | |

| Blue Springs | MO | 2018 | 54,852 | 116.41 | 7.25 | |

| Troy | MI | 2018 | 84,194 | 113.88 | 6.49 | |

| Lakewood | WA | 2017 | 60,310 | 113.37 | 7.50 | |

| Fresno | CA | 2018 | 526,037 | 112.91 | 7.50 | |

| Clearwater | FL | 2018 | 115,476 | 111.18 | 6.99 | |

| Lee’s Summit | MO | 2018 | 97,123 | 110.99 | 7.25 | |

| Ballwin | MO | 2017 | 30,207 | 110.63 | 7.25 | |

| Middletown | CT | 2018 | 46,287 | 109.33 | 7.00 | |

| Lower Merion Twp. | PA | 2017 | 59,021 | 109.01 | 7.20 | |

| Danville | VA | 2018 | 41,022 | 108.78 | 7.00 | |

| Westminster | CO | 2018 | 113,479 | 108.21 | 7.50 | |

| Cape Girardeau | MO | 2017 | 39,298 | 106.74 | 7.25 | |

| Woodlands Twp. | TX | 2017 | 109,608 | 106.45 | 7.00 | |

| Riviera Beach | FL | 2018 | 34,674 | 104.14 | 7.24 | |

| O’Fallon | MO | 2017 | 87,544 | 104.11 | 7.25 | |

| Shelby Charter Twp. | MI | 2017 | 79,152 | 103.51 | 7.50 | |

| Brentwood | TN | 2018 | 42,593 | 103.37 | 7.25 | |

| Janesville | WI | 2018 | 64,565 | 102.93 | 7.20 | |

| West Bend | WI | 2018 | 31,590 | 102.93 | 7.20 | |

| Brookfield | WI | 2018 | 38,770 | 102.93 | 7.20 | |

| Wentzville | MO | 2017 | 39,378 | 102.73 | 7.25 | |

| St Peters | MO | 2018 | 57,146 | 102.42 | 7.25 |

Source: Merritt Research Services, LLC * Most recent audit refers to either the FY 2017 or FY 2018 City C AFR audits. Pension plan audit years often lag by one from the city audit due to preparation/measurement timing differences.

A Cautionary Note

Much to their credit, cities with well-funded pension plans can look forward to less uncertainty relative to potential tax increases and threatening budget squeezes to offset the possibility of future economic downturns or pension actuarial assumptions that are not realized. Best practice in public finance calls for organizations with defined pension plans to have match their pension liability amortization schedule with the time in which a public employee is expected to be providing active services to a community. When pensions are underfunded, the burden is more likely to fall onto the next generation of city taxpayers. That’s a big reason why an optimally appropriately funded pension program makes sense in the long-term and poses the least stress to cities at the end of the day.

Although full pension funding is ideal, some caution is always advisable if the funding ratio is artificially propped up by mistaken actuarial assumptions, like the investment discount or mortality rates. So too, observers have to be careful about the use of pension bonds , especially if they don’t provide strong assurance of a complete package to reduce the overall pension liability. Pension bonds don’t necessarily relieve financial stress in the long run if they just shift the risk to bondholders since debt service is just as much of a future fixed cost burden as pension contributions, maybe even more so. Lastly, if a community covers its pension costs fully and underfunds essential services or infrastructure requirements, there are obvious potential negative implications sooner or later.