Municipal Bond Audit Times Show Slight Improvement Since 2015 But Most Still Late to the Table — The County, State and City Sectors are the Least Timely

By Richard A. Ciccarone

Municipal bond analysts and investors are accustomed to waiting a lot longer for municipal bond financial audits to be completed after the close of the fiscal year than they would on a corporate bond. While public corporations are required to file an annual audit within 60 to 90 days after the close of the year, municipal bond borrowers often finish their audited annual reports in close to twice that time and a large number take even much longer.

While investors need the audit documents for credit evaluation and securities pricing purposes, they are not the only stakeholders that have a need to see timely audited financial reports. Governing boards associated with public bodies and not-for-profit organizations need to review the audits in order to fulfill their duty for proper oversight. Like municipal bond analysts and investors, they are better able to respond to issues disclosed in an audit if the documents are timelier. Although this issue has been lingering for decades, the time it takes to complete and sign an audit after the close of the fiscal year hasn’t changed much over the last ten years.

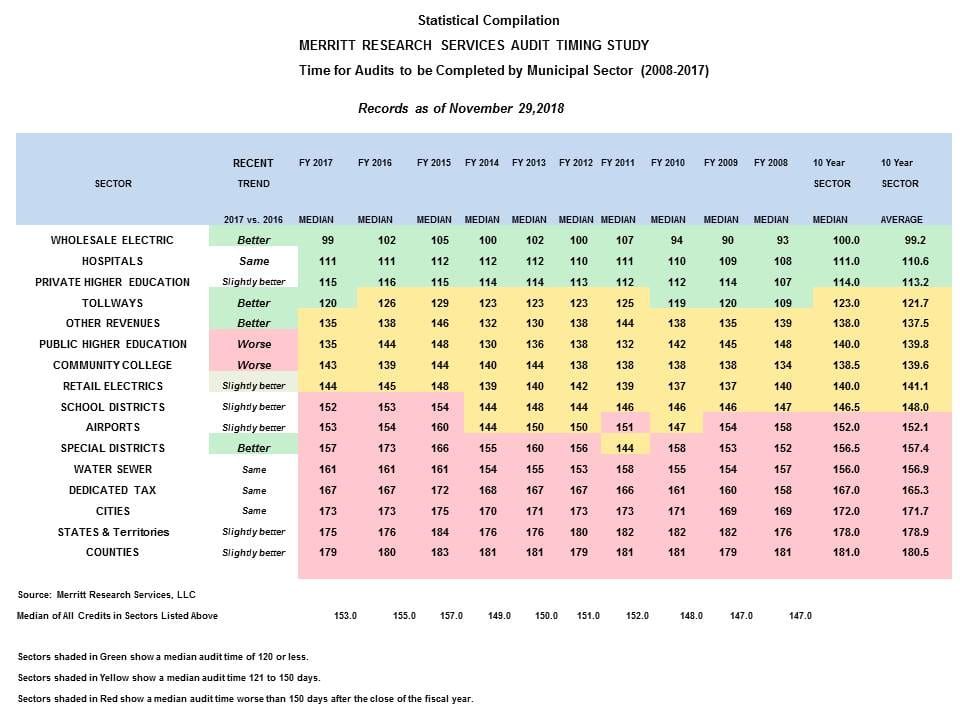

Merritt Research Services, LLC, an independent municipal bond credit data and research company based in Hiawatha, Iowa and Chicago, Illinois, has been tracking the time it takes municipal bond borrowers to complete their audits since Merritt Research released its first report in 2010. Its latest findings looked at over 10,500 Fiscal Year 2017 audits by credit sector and over 110,000 audits since 2008.

The Latest Results

The latest analysis focused on 2017 audits found a modicum of good news in that there was a modest improvement in completion time rates over the past two years as governmental audits have made the adjustments to more detailed pension reporting in line with changes in GASB rules 67 and 68 that occurred mostly in the 2015 audits. Audits form non-governmental municipal bond borrowers, such as power agencies, hospitals and private universities, finished much faster than those for governments.

As has been the case in other years, the median completion time for reports related to governmental type muncipal bonds still hovers between 170 and 180 days. That’s still a long way from the target reporting times in the corporate bond market and well below what the municipal bond industry considers to be a muni guideline of 120 days.

Merritt Research’s latest report continues to show that certain types of municipal bond borrowers, mostly associated with corporate like enterprise entities and not-for–profit organizations (issued under the IRS 501c-3 code), are consistently faster to finish their audits than the governmental state and local governmental sectors. These non-governmental issuer sectors have median times which range from 99 days to 161 days.

Consistently placing fastest on the list of all municipal bond credit sectors are (1) public power wholesale electric agencies (also known as joint action agencies and quasi-government enterprises), (2) hospitals, (3) private higher education institutions and (4) Tollroads. Each of these sectors show a median audit completion time of 120 days or less, passing the unofficial municipal bond guideline most frequently cited as best practice.

Audit Timing Trends by Municipal Bond Credit Sectors Source: Merritt Research Services, LLC

The Fastest Reporting Sectors for Fiscal Year 2017

Public Power Wholesale electric audits achieved the best sector reporting time, boasting a median completion time of 99 days after the close of the fiscal year. Bonneville Power Administration, which registered an extremely low audit time of 27 days for FY 2017, may not be the perfect example of the municipal bond market since it is technically a federal power agency that serves as a wholesale electricity provider to municipal retail electric entities as well as other municipal joint action agencies and co-operatives. Nevertheless, it is worth mentioning because it may be the fastest audited reporting agency associated with any federal government department or agency.

The wholesale electric sector has the distinction of holding the best showing of all municipal credit sectors when it comes to the percent of its entities that report audit completions in 120 days or less. In FY 2017 with 88.6% of all wholesale electric entities able to get the job done, up from 68.5% in 2014. Even more impressive is that forty-four percent of this sector was able to report its audits in 90 days or less.

Hospitals, which often carry higher interest rates since many consider them as one of the riskier major credit sectors in the muni market, annually place nearly as well as wholesale electric entities in the audit time contest. As a group, they recorded a median audit completion time of 111 days, the same as the prior year. Since 2008, the hospital audit time median has remarkably ranged between 108 to 112 days. The hospital category includes both large behemoth hospital systems to small independent community hospitals. In FY 2017, the three best reporting hospital entities were the Kaiser Foundation Health Plan (CA) at 45 days, Mercy Health Corporation (IL) at 46 days and the Mayo Clinic (MN) at 50 days. As a group, 70% of all hospital sector municipal bond borrowers finished their audits in 120 days.

The Private Higher Education sector took the third best sector finish for fiscal year 2017 with a median audit time of 115 days. Again, this sector has consistently completed its audits in a narrow range of between 107 and 115 days since 2008. A university that stands out every year as being the timeliest is Syracuse University in New York. This year it finished its audit in 41 days, which is actually its slowest time in the past ten years. Sixty-three percent of the Private Higher Ed sector was able to get its 2017 audits finished within 120 days.

The Tollroads sector showed the best gain of any of the categories by improving its median from its already good audit time level of 126 days to 120 days. Fifty-one percent of the sector completed their audits in 120 days.

The Slowest Reporting Sectors in Fiscal Year 2017

On the other side of the speed continuum were the main governmental sectors – counties, states and cities.

Despite their absolutely disappointing finish times, each of these sectors showed a modest improvement and reduction in their median audit times from last year and further progress since 2015. That’s the year in which governments were required to apply more detailed pension accounting information in line with the new Governmental Accounting Standards Board (GASB) 67 and 68 rules concerning pension accounting that went into effect. The implementation period often caused these governmental sectors to take more time to finish the audit. The Fiscal Year 2017 audit times appear to indicate that the transition period has transpired and the numbers again leveled off.

It will be interesting to see if they can hold that progress in FY 2018 as they adjust again to new GASB rules, this time dealing with Other Post-Employment Benefits.

The County Sector showed the slowest financial reporting as a group. The median sector audit time came in at 179 days, several days better than two years ago and one day better than last year, but still nothing to boast. Only 4.6% of all counties finished their audits in 120 days, the worst group performance of any sector. The best county audit time belonged to Santa Barbara County, CA with an audit time of 56 days. The runner up was Somerset County, TN at 62 days. The slowest reported county was Darlington County, GA at 426 days.

States & Territories, which was the second slowest sector in 2017 and the tardiest of all sectors in the previous two years, inched up a notch with a median audit time of 175 days. Only 5.7% of this sector was able to have their audits signed for completion within 120 days.

The best state in FY 2017 was the State of Michigan, which got the job done in 97 days. The runners-up were the District of Columbia and New York at 116 and 117 days, respectively.

Alabama turned in the tardiest performance by a state for the second year in a row, clocking in at a completion time of 426 days; better than the time span in 2015 when it finished its report in 565 days. New Mexico placed number two from the bottom for FY 2017 at 335 days while New Jersey took the third slowest spot at 272 days. With audits from two territories still not completed, either Puerto Rico or the U.S. Virgin Islands will ultimately “win” the distinction of being the most unpunctual state or territory to log in their FY 2017 audit numbers. The odds “favor” Puerto Rico; its most recent audit applies to FY 2015 which it finished in 1,095 days after its fiscal year ended.

The City Sector was the third slowest sector, albeit the best, among the major governmental categories. Its median audit time was 173 days. Like states and counties, it has fallen among the bottom three in each of the last ten years. It tied states for having the same 5.7% of signed audits within 120 days of the end of the fiscal year. The three fastest reporters in the city category belonged to New Jersey cities; however, they all had qualified opinions that are not in compliance with GAAP standards consistent with GASB. For that reason, the real honors go to Eastchester, NY at 58 days, followed by Florence, KY and Kettering, OH at 73 and 74 days, respectively.

Among large cities, the winner is the perennially fast reporting city, Columbus, OH at 88 days, its 9th straight year at 120 days or less. Pittsburgh is due an honorable mention at a 117 day audit time for its fifth straight year at 120 or less. Then, as evidence that governmental reporting rules, which some consider as more burdensome as corporate Financial Accounting Standards Board (FASB) rules, cannot be used as a simple excuse for late audit times, New York City completed its audit in 122 days, its 11th straight year at 123 days or less . That’s a major achievement for a complex governmental unit with multiple component units to consistently get the job accomplished. As they say, if you can do it in New York, you can do it anywhere.

Some governments are allowed by their individual states (e.g. New Jersey) to not comply with Generally Acceptable Accounting Principles (GAAP). When that happens, auditors are expected to disclose that fact and the accounting method that the audit is using. By GAAP auditing standards, non-GAAP audits are given a qualified opinion and not deemed comparable to other governmental type entities. Audits receiving a qualified opinion are not unlike a “buyer beware” type notice.

Closing Thoughts

Audit timeliness is a simple, common sense principle based on the expectation that accountability and transparency are best achieved if audited financial reporting is swiftly dispatched. That should hold true not only as a standard for responsible government but also for investors and taxpayers.

There’s an added fiduciary responsibility for municipal bondholders in that late or stale audits inhibit accurate bond pricing and cloud assessments of risk. The absence of significant improvement in the overall speed in which are audits are signed and delivered begs the question as to why the market is not imposing a greater penalty on those that consistently are late to report.

Richard A. Ciccarone, President & CEO of Merritt Research Services, LLC*

© Merritt Research Services, LLC is an independent municipal bond data and research provider, distributed by Investortools Inc.’s CreditScope software package. Established in 1986, Merritt Research is the first and the oldest subscription based municipal bond credit database and software package available in the municipal market.