A Few Quick Points About City Pension Funding…

by Richard A Ciccarone

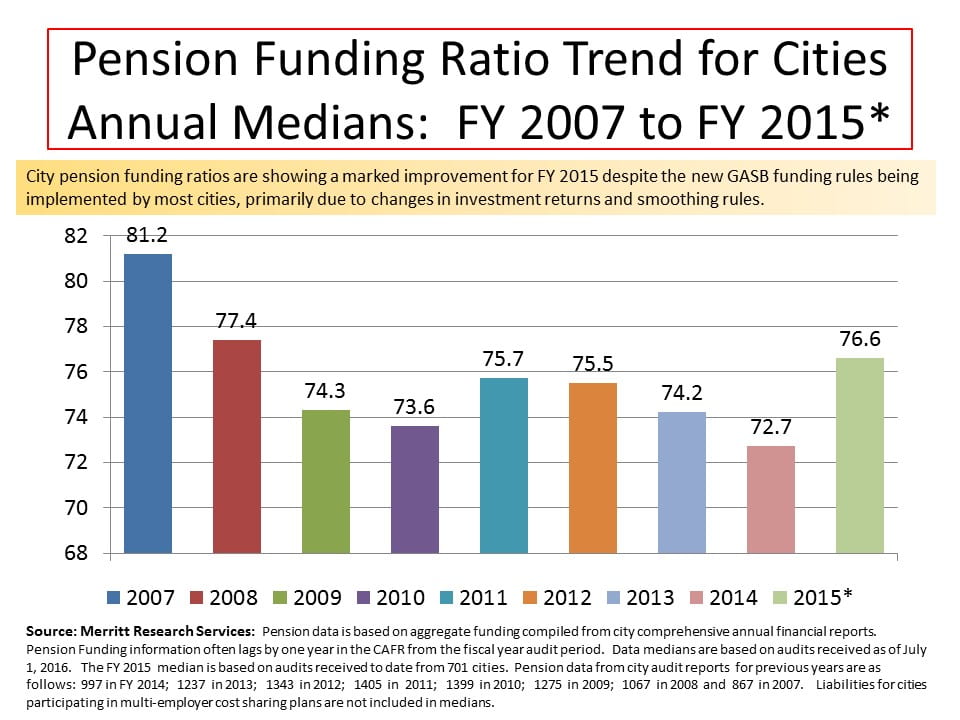

- Based on audited results from 701 cities received to date by Merritt Research Services, City single/agent pension funding ratios showed a marked improvement in FY 2015 compared to the previous year. As of July 15, 2016 the median city pension funding ratio for FY 2015 stands at 76.6% compared to only 72.7% in 2014. That’s the best pension median for cities since 2008, the first year of the Credit Crisis.

- The more upbeat pension 2015 funding numbers are particularly significant because they are based on the new GASB 67 and 68 pension rules which were implemented for the first time by most cities. Among the many changes in pension accounting rules, the concept of smoothing asset valuations was eliminated by most governments so that better overall market returns from 2013 to 2015 were reflected in the numbers.

- Pension reforms have occurred in many cities over the last several years, which probably accounts for a portion of the improvement in the funding ratio.

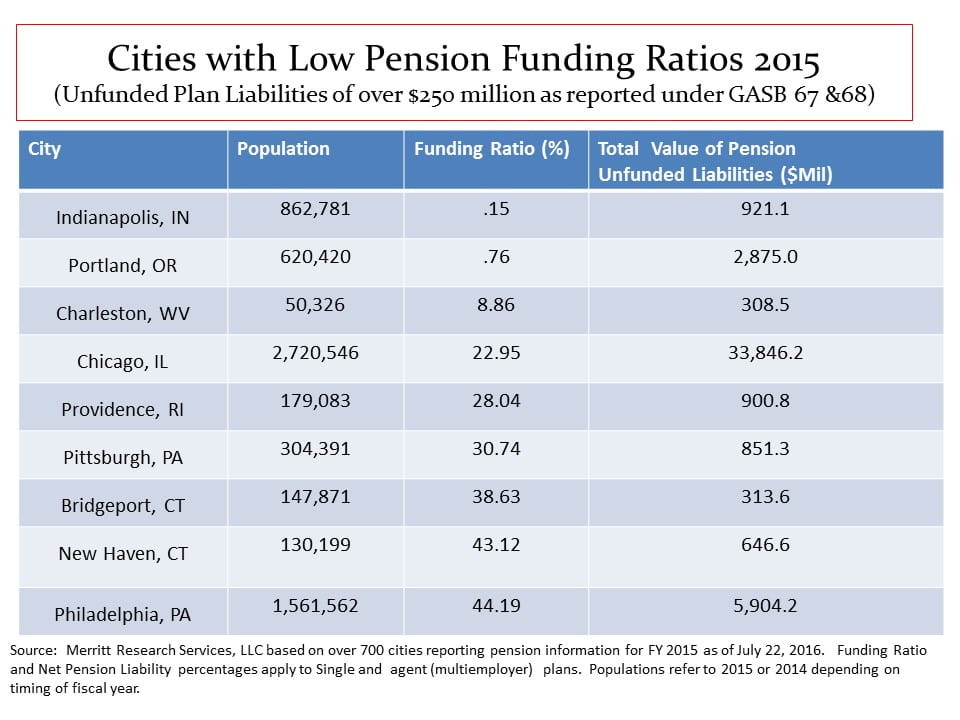

- The GASB rule change that had the most potential to negatively impact funding ratios was the requirement that a lower discount rate at a 20 year tax exempt rate (under 4%) would be required for the portion of any government’s liability that exceeded the expected assets available to pay benefits. However, relatively few cities projected results that placed them in that position. The city of Chicago reported that two of its four plans triggered the lower blended discount rate. Its 2015 aggregate city funding ratio reported by Merritt Research was 22.95%, which is one of the weakest of all cities in the nation.

- Among the weakest city pension funding ratios, shown in the chart below, are Indianapolis, Portland and Charleston, WV. The city of Portland levies a limited tax property levy to fund its annual requirement. In the case of Indianapolis, their annual comprehensive annual financial report notes that “the State of Indiana, in 2008, agreed to reimburse the cities and towns of Indiana for pension costs for members of the pre-1977 pensions plans effective January 1, 2009. Therefore, although unfunded, these pension benefits which represent $922 million of the total net pension obligation [includes proportionate share of liability amount to Indiana cost sharing plan] will be covered by the State of Indiana”. Charleston uses primarily a pay-as-you go approach for funding. All three cities use a lower discount rate in line with new GASB discount rate rules.

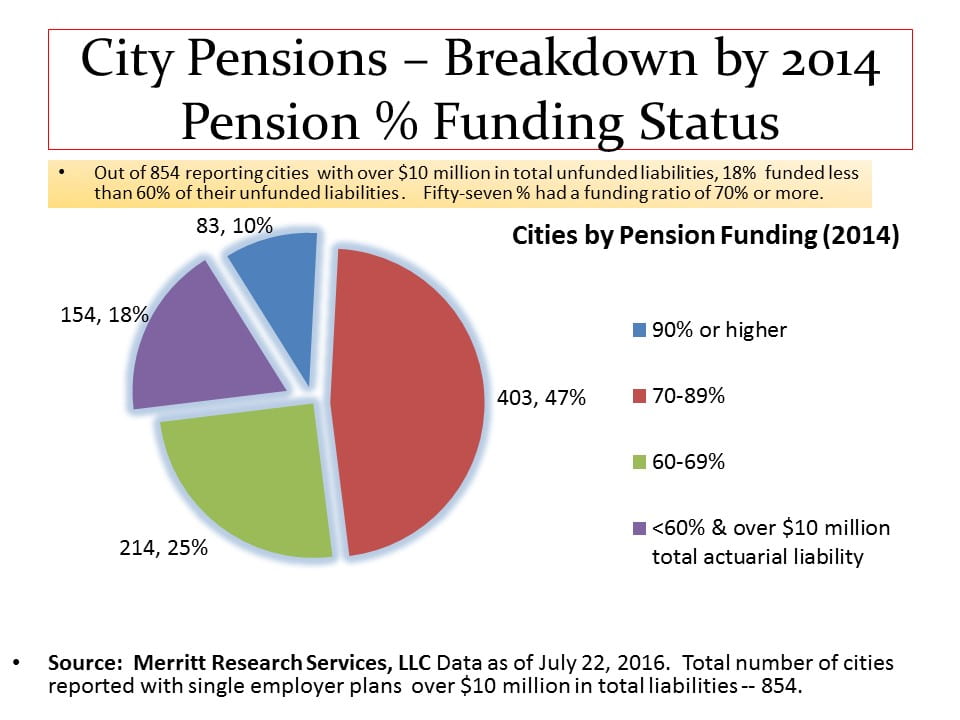

- Prior to the new GASB rules, implemented in 2015 for most governments, about 10% of all cities with total pension liabilities of over $10 million had funding ratios of 90% or more. On the other hand, 18% had funding ratios under 60%. (See chart below)

Richard A Ciccarone, Co-Publisher of MuniNet and President of Merritt Research Services, LLC