Egleston Children’s Hospital in Atlanta circa 2011

Image from: https://commons.wikimedia.org/wiki/File:Henrietta_Egleston_Hospital_for_Children.JPG

License: https://creativecommons.org/licenses/by-sa/3.0/deed.en

Featured Bond – Week of July 15, 2019: Children’s Healthcare of Atlanta Inc. $915 Million in Revenue Bonds

Overview

Children’s Healthcare of Atlanta is borrowing $915 Million through negotiated sale during the week of July 15. The proceeds are to be used to develop the North Druid Hills campus and to refund the Series 2009 and Series 2017 Bonds issued by the Development Authority of Fulton County. The preliminary issuers of the 2019 Bonds are Brookhaven Development Authority, DeKalb Private Hospital Authority, and the Development Authority of Fulton County. The bonds are rated Aa2 by Moody’s and AA+ by S&P.

More About The Bonds & Children’s Healthcare of Atlanta

The bonds are split into four Series – 2019A through 2019D. Series 2019A is $753 million in tax-exempt fixed rate bonds with issuer Brookhaven Development Authority. Series 2019B is $84 million in tax-exempt fixed rate bonds with the issuer DeKalb Private Hospital Authority. Series 2019C is $77 million in tax-exempt fixed rate bonds with issuer Development Authority of Fulton County, and then Series 2019D is $109 million in tax-exempt variable rate bonds with issuer Brookhaven Development Authority.

Children’s Healthcare serves 9 out of 10 pediatric inpatients in the Atlanta MSA and 6 out of 10 pediatric inpatients in the State of Georgia. It is one of the highest rated healthcare credits in the nation. The North Druid Hills project, where proceeds from the 2019 bonds are being used, will address capacity needs driven by projected pediatric demand. The demand requirements are outpacing the resources existing at Children’s Hospital’s Egleston and Scottish Rite locations in Atlanta. The newly-developed North Druid Hills campus can accommodate long-term needs. The new hospital facility will be a 20-story 446-bed pediatric acute care facility and is expected to start serving patients in 2025.

Security for the Bonds

The bonds of each 2019 Series are special limited obligations of the issuers and are payable solely from funds pledged under each respective bond indenture, a pledge of certain rights of the issuers under and pursuant to each respective loan agreement. The bonds are not a debt of the State of Georgia or any subdivison thereof. The issuers have no taxing power.

These details and more on purposes, security, risks and other matters pertaining to these Children’s Healthcare of Atlanta Inc. Revenue Bonds can the found in the official statement, provided by MuniOS. After registering, if needed, visitors can link directly to the official statement as well as an investor’s roadshow by searching for Children’s Healthcare of Atlanta.

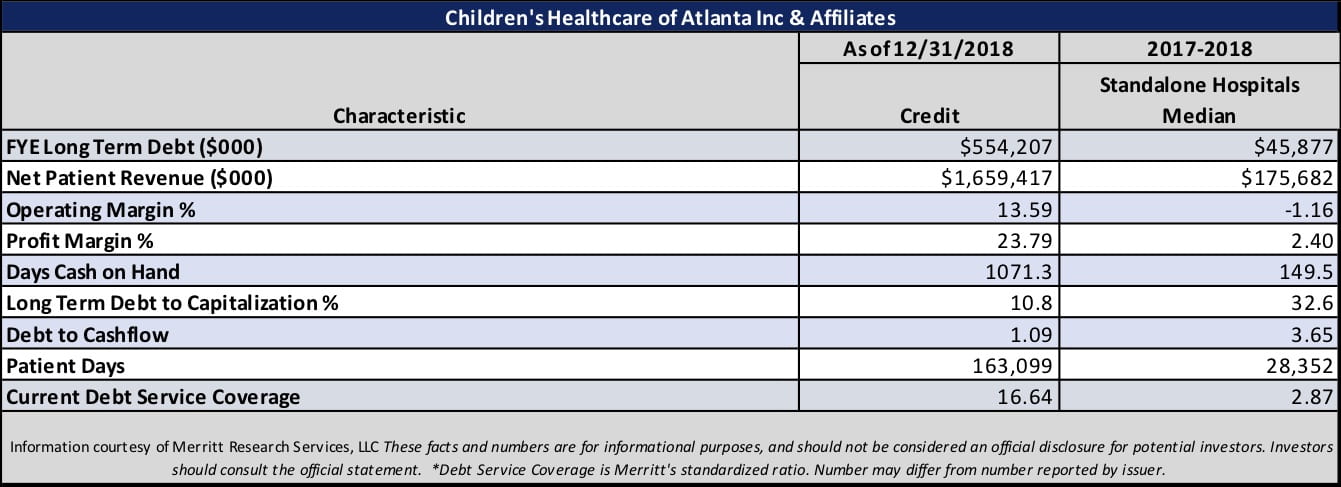

Statistical Snapshot: Children’s Healthcare of Atlanta Inc. Selected Financial and Economic Indicators

Children’s Healthcare of Atlanta Inc. financial snapshot as of December 31, 2018 Fiscal Year Audit. Source: Merritt Research Services, LLC

Provided above is a quick snapshot of financial characteristics of the Children’s Healthcare of Atlanta Inc. along with the medians for other financial hospitals, courtesy of Merritt Research Services, LLC. Merritt has many of the sector medians publicly available and regularly updated on their Benchmark Central page. (Merritt believes the data to be reliable but does not make any representations as to its accuracy or completeness).

In addition to the Merritt information related to the featured bond, more information can be found on our municipal bond calendar, city, state, and county pages.

These facts and numbers are for informational purposes, and should not be considered an official disclosure for potential investors. Investors should consult the official statement. None of the information provided should be construed as a recommendation by MuniNet Guide, MuniNet LLC, Merritt Research Services LLC, or any of their employees. Information and analysis is for informational purposes only.

Potential investors should rely only on the official documents and figures provided in the official statement (prospectus). Although the numbers presented in this summary are primarily derived from public documents, including issuer audits, issuer reports and other public sources such as federal reporting agencies , they are not intended to replace official information presented in connection with the bond sale. Medians may differ from official sales documents due to methodology or survey base variances.