We cannot avoid economic cycles but history of financial stability points the way

In the U.S.A., financial challenges and difficulties in balancing a government budget are not so much caused by the desire to spend more than tax revenues currently generate but rather by economic cycles such as panics, recessions and depressions. The cycles are exacerbated by unfunded pension obligations that are not sustainable and affordable as well as the adverse effects of failing to fund essential services and needed infrastructure at an acceptable level. The healthy economy of a state or local government goes hand in hand with full funding of essential services and needed infrastructure improvements and making sure all costs, including labor and pension obligations, are sustainable and affordable. But will the adverse affects of digital, shared economy and artificial intelligence revolution prevent the needed funding of essential services and infrastructure improvements?

Need to address the systemic problems of the past that caused financial distress, namely the tax policy for sufficient revenues and methods of preventing over-leveraging

Other countries that have suffered the need for a debt restructuring due to lack of tax revenue or over-leveraging have generally repeated the process numerous times with band aids rather than a permanent fix because they merely reduced debt without addressing the systemic problems that caused the financial distress. States and local government should always strive for the permanent fix as opposed to the band aid.

Balanced budgets require services and infrastructure at the level desired

The state and local governments in the U.S.A. have a long history of financial credibility having learned that quick fixes and failure to maintain governmental services and infrastructure at an acceptable and desired level result in a loss of businesses and individual taxpayers with the accompanying fiscal distress.

The state legislatures have assisted in balancing the budget with needed legislation

State legislatures have assisted state and local governments by passing legislation that (i) limits debts and taxes, (ii) provides financial oversight and assistance to those who need it, (iii) assures and requires funding of needed services and infrastructure at the level desired, (iv) respects the principles of government financing and uses statutory liens and special revenues to reduce the cost of borrowing and reinvests in the state and local governments and (v) encourages reinvestment in the state and local governments and creation of new, good jobs and business development.

The need to reinvest in state and local governments as party of an acceptable tax policy:

The $3.6 trillion price tag and cost of delay. The American Society of Civil Engineers (“ASCE”), in its 2013 Report, estimates the cost to maintain infrastructure at a passable level will be $3.6 trillion by 2020 or about 4 times the annual tax revenues for all state and local governments. In 2009, ASCE’s number for the next 5 years was $2.2 trillion. Inattention has caused the number to increase by $1.4 trillion in 5 years. ASCE’s 2017 Report stated the cumulative infrastructure funding needs based on current trends extended to 2025 is $4.59 trillion to have passable infrastructure. Estimated funding for this infrastructure has a gap of over $2 trillion. ASCE discovered in its 2016 economic study “Failure to Act Closing the Infrastructure Investment Gap for America’s Economic Future” that the failure to do necessary infrastructure improvements in the U.S.A. will cost the county $3.9 trillion in losses suffered to the GDP by 2025, $7 trillion in lost business sales by 2025 and $2.5 million in lost American jobs in 2025.

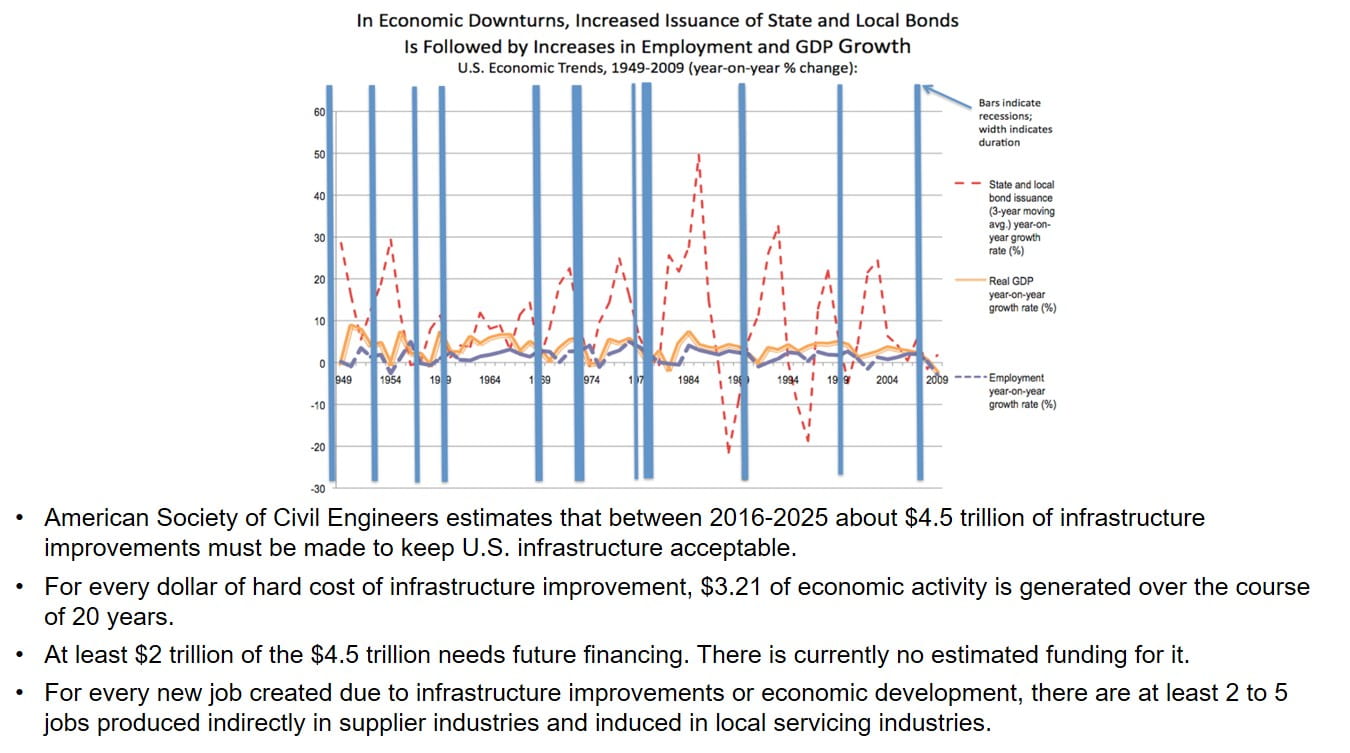

Historically state and local government increased reinvestment after economic downturn. Continued borrowing is required to fund needed infrastructure and stimulate the economy as demonstrated by increased borrowing after each economic downturn since 1949, except the last one (2008).

CHART 1

Economic growth and job multiplier. Reinvestment in needed infrastructure improvements creates increased GDP. As studies have shown, $1.00 of hard infrastructure costs adds $3.20 over 20 years to GDP growth. Further reinvestment in infrastructure translates into year to year growth of the number of employed workers and GDP growth given the economic stimulus and job multiplier. (Every new job creates service jobs that increase productivity indirectly. This can range from two or three to four or more new jobs depending upon the industry it is created in.) Examples of economic development approaches are set forth in next section on foreign trade zones and industrial parks. The stimulation of economic growth through programs that attract new business to move into financially-challenged states and municipalities and create new jobs increase the tax revenues that help resolve the financial distress and lead to financial recovery of the municipality or state.

State and local government pension fund’s status:

There are approximately 4,000 public sector retirement systems for state and local governments in the United States with $3.8 trillion in assets, 14.4 million current employees, 9 million retirees and annual aggregate benefit distributions of $228.5 billion. The estimated amount of pension underfunding for states and local governments is estimated to exceed $1 trillion. This unfunded liability for pensions of over $1 trillion can be compared to the estimated FY2016 revenue of $3.3 trillion for state and local governments.

Many state and local governments have no current pension fund problem or have resolved it

It should be noted that the vast majority of states and local governments have or will successfully address public pension issues without extensive prolonged disputes or litigation.

The aging population and possible future economic downturn are reasons to be vigilant no matter the current conditions of the pension fund

Those over 65 years of age in the United States constitute an increasing percent of the population, namely 14.8% of the 2015 population, which is expected to grow to 20.9% by 2050. Likewise, the working years of 18-64 of age are expected to be reduced as a percent of population, namely from 62.2% in 2015 to 57.6% in 2050. This results in about 40 million more people over 65 as potential retirees.

While the USA percentage of population over 65 in 2050 (20.9%) is lower than many other developed countries, such as Europe at 26%, China at 24% and Japan at 33%, it is still a concern. Likewise there have been 11 economic downturns since 1949, about one every 7 to 10 years, so we now are facing the probability of an economic downturn in the next few years since the last downturn was 2008. Economic downturns result in losses on pension fund investments and less revenues available to state and local governments to address the issues.