In Washington, the GOP Targets Big Changes to the State and Local Tax Deduction; What are the Impacts?

by Jeffrey L Garceau

The Republicans in the U.S. House of Representatives have released their long-awaited tax reform plan on Thursday. Tax-reform will affect virtually the entire economy, but MuniNet’s core focus on state and local governments, economies, and communities warrants special attention to their planned reform of the state and local tax deduction. The state and local tax deduction allows taxpayers who itemize their deductions to include state and local real estate, personal property, sales, and income taxes from their federally-taxable income. According to the non-partisan Tax Policy Center, in its current form this deduction will cost the Federal Government and estimated $96 billion in revenue in 2017 alone, and $1.3 trillion in the 10-year period from 2017-2026.

The Plan

Once rumored to be possibly repealed outright, and then seen to likely be untouched, the GOP plan instead modifies a tax deduction claimed by nearly 30 percent of income tax filers. According to the GOP plan:

- Specifically, the bill repeals the itemized deduction for state and local income taxes and sales taxes,

and preserves this deduction for state and local property taxes. - State and local property tax deduction capped at $10,000.

The plan states that “Modifying the State and Local Tax Deduction in this manner helps contribute to a simpler, fairer tax code that has lower federal income tax rates for all Americans – regardless of where they live

or whether they itemize deductions. Additionally, it continues to provide important property tax relief for Americans who now face a high property tax burden.”

Are Changes Good or Bad?

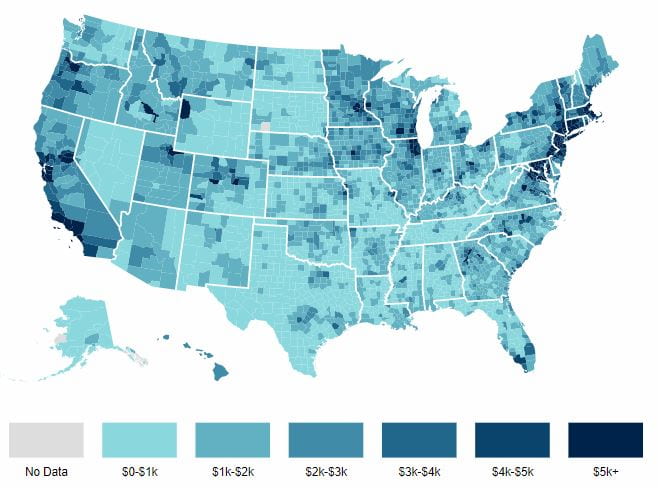

Leading think tanks bring different perspectives to any sort of repeal of the state and local income tax deduction. The Tax Foundation states that the deduction disproportionately benefits high-income taxpayers, with 90 percent of deduction savings going to filers with incomes in excess of $100,000. Further, the tax benefit falls disproportionately on high-tax states, particularly large urban centers. The map below from the Tax Foundation shows the mean deduction taken per tax return in each county in the U.S. A clear concentration of deduction savings in coastal states and the upper Midwest appears.

Mean State and Local Tax Deduction Savings by County

(Source: Tax Foundation)

Source: Tax Foundation // Click to Expand

According to the Center for Budget and Policy Priorities, eliminating the SALT deduction is a bad deal for most Americans. They point out that planned cuts in marginal tax rates and other reforms could benefit higher income people even more than repeal of the state and local tax deduction, thereby giving a net-benefit to high-income households. State and local budgets and borrowing costs may also be impacted, as state and local taxes become more expensive and less popular. As these taxes are presumably used to provide services to residents, the ability of the state or locality to provide services at desired levels could be threatened.

One other argument that gets made is that the state and local tax deduction is a federal subsidy for states with high taxes, incentivizing and supporting those states’ tax burdens. While there is truth to this, it should be noted that many of the states that benefit less from the state and local tax deduction benefit more from the Federal Government in direct aid. The map below, also from the Tax Foundation, shows states by federal aid as a percentage of state general revenue for 2014. A comparison with the map above shows a reverse benefit from federal spending.

Judging the value of the SALT deduction based on whether or not it is fair or unfair to states and localities seems tricky, based on the various ways state or local governments can be labeled as gaining advantages over others through SALT deductions, direct aid, and other tax expenditures. Additionally, the state and local tax deduction will not be repealed or altered in a vacuum; judging federal tax reform needs to be done with a holistic analysis of the complete bill. However, state and local governments have reasons to be concerned.