State Retirement Savings Plans Provide Opportunities for Small Businesses and Their Employees

Offering retirement plans is a widely practiced benefit offering among U.S. employers. However, the vast majority of those plans are offered by large companies with 500 or more employees. Many small businesses do not offer plans, which contributes to the one-third of Americans who do not have access to retirement plans through their employer. When workers are unable to get retirement advice and make contributions through employer provided plans, they are forced to educate themselves and develop saving strategies on their own, or pay advisers out of pocket. This is a barrier to millions of workers who have little or nothing saved for retirement. To help fill this gap, state governments have begun offering retirement plans available to workers who are not offered retirement plans through their employer.

The Problem

Many small businesses do not offer retirement plans, which impacts millions of working Americans. A report by the Federal Government’s Small Business Administration (SBA) from 2009, found that almost 72 percent of workers in small companies (>100 employees) have no retirement plan available through the company.

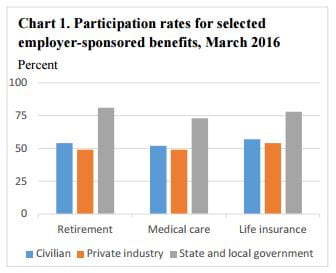

Source: U.S. Bureau of Labor Statistics – Click to Expand

The main reasons smaller businesses are less likely to offer retirement plans than large businesses are the cost of the plans, the regulatory burdens of the plans, the fiduciary responsibilities required of the plan sponsors and a general lack of employer education about the requirements and processes of setting up and sponsoring a plan. Indeed, a lack of education around the importance of saving for retirement and the ability of employees to contribute keeps millions more Americans from even participating from the plans available. The U.S. Bureau of Labor Statistics (BLS) reported in July that only 75 percent of private sector employees take advantage of the retirement savings plans that are available to them through their employers.

The U.S. population is rapidly aging. People are living longer. That means that they will need more resources in retirement. Government will have to provide retirement and old-age benefits like Social Security and Medicare for more people for longer periods of time, straining the fiscal viability of these programs.

America’s aging population is well illustrated by these charts from the Urban Institute. Seniors over 65 and over 85 will not only continue to grow as demographics in total, but also as a proportion of the overall U.S. population.

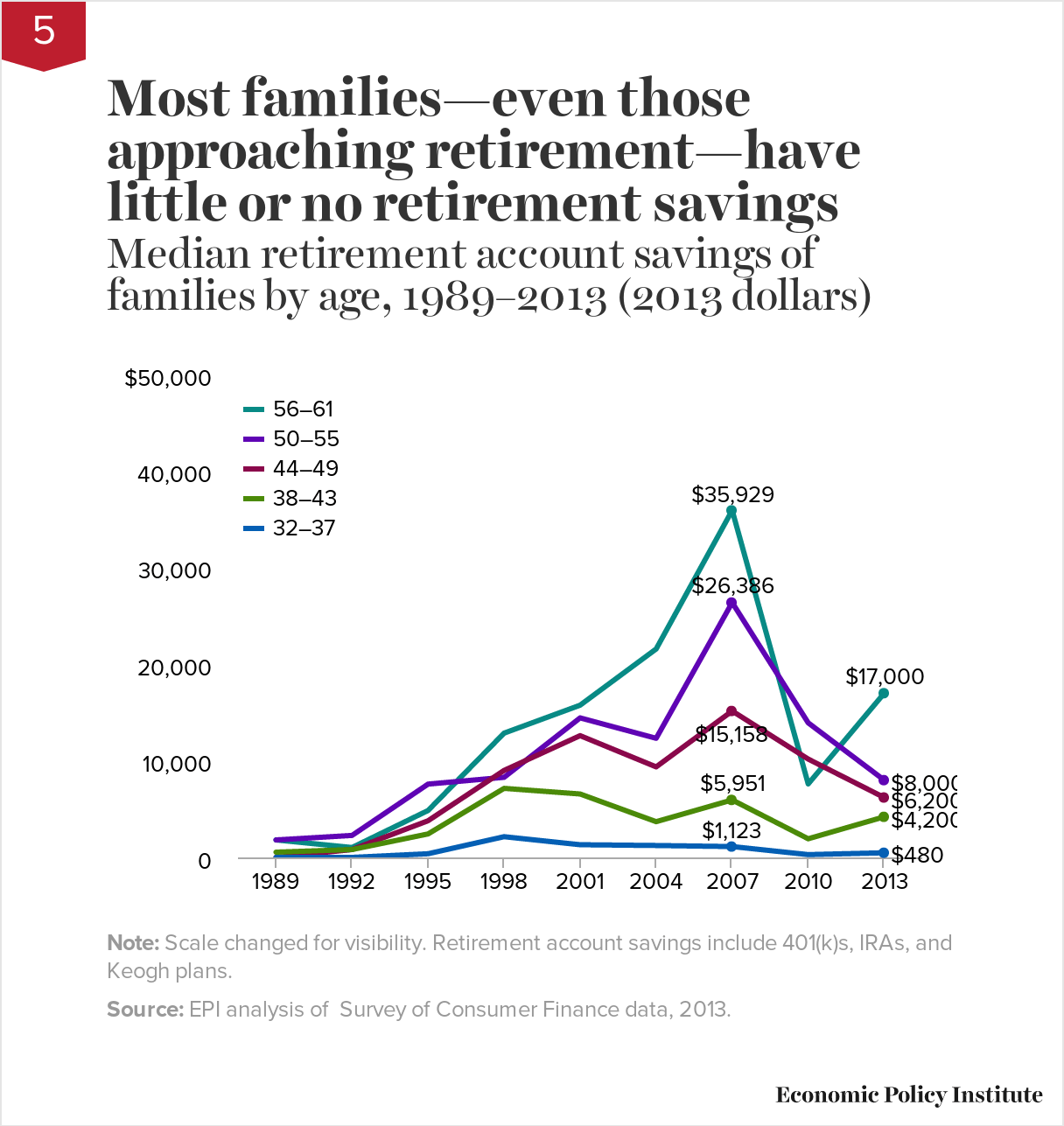

Retirement savings are also alarmingly low for the average U.S. family. The following chart, from the Economic Policy Institute, shows how hard retirement accounts were hit by the Great Recession. They also show that, even near retirement age, and at their peak in 2007, the median U.S. family aged 56-61 had only $35,929 set aside in retirement funds. Now, many of these families may have other assets like their home, and will also likely be eligible for Social Security benefits, but the overall picture is one of people not having nearly enough set aside for their retirement years.

No single government policy or private product or service is going to simultaneously address the issues of people not having easy access to savings plans, people not taking advantage of savings plans that are available to them, and people not saving enough when they do take advantage of such plans. However, some state governments are trying to at least address the first issue, and ensure that people with steady income have easy access to retirement savings accounts.

The Solution?

In order to reach the group of working adults who are not offered retirement plans by their employers, a number of states have passed legislation to form what are commonly referred to as State Sponsored Retirement Plans. The key to these plans is automatic enrollment. Many employer plans automatically enroll the individual to begin contributing an amount of each paycheck into their own retirement account, usually 3% of income. The employee is made aware that this will take place, and has the option to raise or lower their contribution, or to opt-out of the program at any time. Academic research supports that automatic enrollment increases the percentage of people who save for retirement, and can increase the amount saved.

Three states that are currently in the final design phase or implementation phase of these programs, Illinois, California, and Oregon, offer insights into how these programs are managed. They are very similar to common employer-based plans.

Illinois:

- Program implementation is underway, but operations are not running yet; program target is to begin operations by 2018-2019

- Automatically enrolled – Default 3% contribution into Roth IRA

- Program run by independent board

- Accounts pooled and run by private investment company

- Investment fund, contribution amount, and participation can be changed at any time

- Accounts owned individually, and can be moved from employer to employer

- Legislation forbids program to establish employer or state liability under federal Employee Retirement Income Security Act (ERISA).

Oregon

- Pilot group to start participating July 1, 2017. Gradual implementation after that to be determined

- Automatically enrolled – Default contribution and plan still to be determined

- Plan choice and participation can be changed at any time

- Based on best practices, the automatic payroll deduction will gradually increase over time, setting aside more of your income as you near retirement

- State and employers are free from any liability of guaranteed returns or benefits. Investments are at employee risk

California

- Automatically enrolled – Default contribution is 3%

- For first three years, funds will be investment in low-risk Treasury securities and other secure investments

- Further design of investment plans and options is being worked out by management board

- Ability to adjust contribution, and enrollment can be ended any time. Re-enrollment to be allowed during open enrollment period no less than every two years

- Individually owned plans that can be moved from employer to employer

- Neither employer nor the state holds any liability of returns or benefits

- Employers requirements:

- Enable employees to make an automatic contribution from their paycheck into their Secure Choice Account.

- Transmit the payroll contribution to a third party administrator to be determined by the Board.

- Provide state developed informational materials about the program to their employees.

- Program will not cost taxpayers anything. Management costs paid by small fee taken from worker contributions

Each plan exempts any and all employers who offer at least one retirement option to their employees. They mandate businesses that do not offer, with details of business size and compliance window varying by state. Employers are not required to and, in the case of Oregon, are explicitly forbidden from contributing to the retirement plans. Employers will have to bear some cost burden of distributing educational materials and facilitating direct deposits into employee retirement accounts.

Pros and Cons

Proponents of these programs say that not only will retirement saving increase, but it will reduce the burden on local, state and federal government programs they would have otherwise required had workers failed to save. Opponents of the plans worry about the bureaucratic burden on employers, and workers living paycheck-to-paycheck overwhelmingly opting out. Both would cause resistance to and decrease the benefits of the plans. Employees may even be angered if they do not understand the optional component of the program.

The National Association of Insurance and Financial Advisors officially opposes these programs, saying that they are unnecessary when the private market already offers numerous alternatives. They acknowledge that not enough people are saving for retirement or saving enough for retirement, but believe “states would be better served by using scarce state resources for education and outreach efforts designed to educate their citizens about the importance of saving for retirement, rather than implementing their own costly state-run plan.”

The employer mandate is a potentially problematic aspect of this policy. Although the government does pick up much of the costs of setting up the program that will be recouped by participant fees, there is an administrative cost to employers, who are required to set up direct deposit, administer materials, and generally relay information between the program and the employee. Some businesses may welcome this as an affordable alternative to private plans that they would gladly offer their employees if they financially were able to do so. Other struggling businesses may be crippled even by modest administrative costs.

Certainly management fees and the fund pool based upon the number of participating workers and the size of their contributions is a key to whether these programs are successful. There is evidence that these programs will increase the overall savings rates of working Americans, but not all citizens pay into these programs. Will the sector of the population that isn’t offered a retirement plan from their employer largely opt out? If the reason they have not sought retirement plans themselves is an issue of affordability, that may very well be the case. Even a sizable minority of eligible workers opting out may be enough to render these programs no longer economically viable. If that happens, do state governments simply dissolve the plans, return the money currently invested to the participants, and leave them on their own? There could be a lot of political pressure for state governments to subsidize these plans, once they have become ingrained as a service offered by the government. ‘Mission Creep‘ is a legitimate concern for business owners and taxpayers.

A further concern is the nature of the management of these programs, including the politicization of the management process. States have shown to struggle in managing their own public employee pension funds. Illinois’ program is managed by an independent board, that consists of the Illinois State Comptroller and Treasurer, as well as private business leaders. The funds will be managed by a private investment company. Which company, and the decision making process for choosing that company, are to be determined.

Oregon’s board consists of the State Treasurer, a member of the State House and Senate, appointed by leadership of each body, and the following Governor appointments: a representative of employers, a representative with experience in the field of investments, a representative of an association representing employees, and a public member who is retired. The only detail on the actual fiscal management is that it will be ‘professionally managed‘.

In California, the board consists of the State Treasurer, Director of Finance, Controller, an individual with retirement savings and investment expertise appointed by the Senate Committee on Rules, n employee representative appointed by the Speaker of the Assembly, a small business representative appointed by the Governor, a public member appointed by the Governor, two additional members appointed by the Governor. The California program allows the State Treasurer to invest funds with the board of a California public retirement system or with private money managers.

The argument that government can best solve this problem simply by raising more awareness is unconvincing. There are already ample efforts and resources dedicated by both private and public actors to educate the public about the importance of saving for retirement, and saving early. If current resources dedicated to educating the public on these matters is inadequate, it seems unlikely new education efforts by state governments would do much to improve saving.

Some greater policy step than information is required to solve this issue. However, the policies as currently conceived leave a lot of reasons for concern. One alternative is to look at the structure of 529 plans, which are sponsored by all state governments and allow advantageous options for saving for college. These options are administered directly by the government, so there is no employer mandate or costs to small businesses. There is also no mandate of individuals to invest, so while the plans offer greater individual choice, they fail to address the issue of people not saving when it is financially responsible to do so. Some states also guarantee investments in 529 plans, which increases liability in the result of a deep recession or financial mismanagement. The current proposals for Retirement Savings programs do not have this government liability. More information on 529 plans can be found here, provided by the U.S. Securities and Exchange Commission.

Finally, there is a strong argument to be made that other community investments, such as education and infrastructure, are more pressing and would provide greater returns, and are more deserving of increased dedication of government resources.

In addition to clicking on the links above to specific state plan websites, more information on these programs and saving for retirement in general can be found at this excellent resource center, provided by AARP.

by Jeffrey L Garceau