Part V of James Spiotto’s Series on Fiscal Distress Myths & Realities: Factors That Have Helped Prevent State and Local Government Defaults and Municipal Bankruptcies

Myth: There is Nothing Special About State and Local Governments that Would Prevent Defaults and Bankruptcies

Reality: There are Numerous Factors that are Aimed at Preventing State and Local Governments from Defaulting or Filing Chapter 9 Bankruptcies

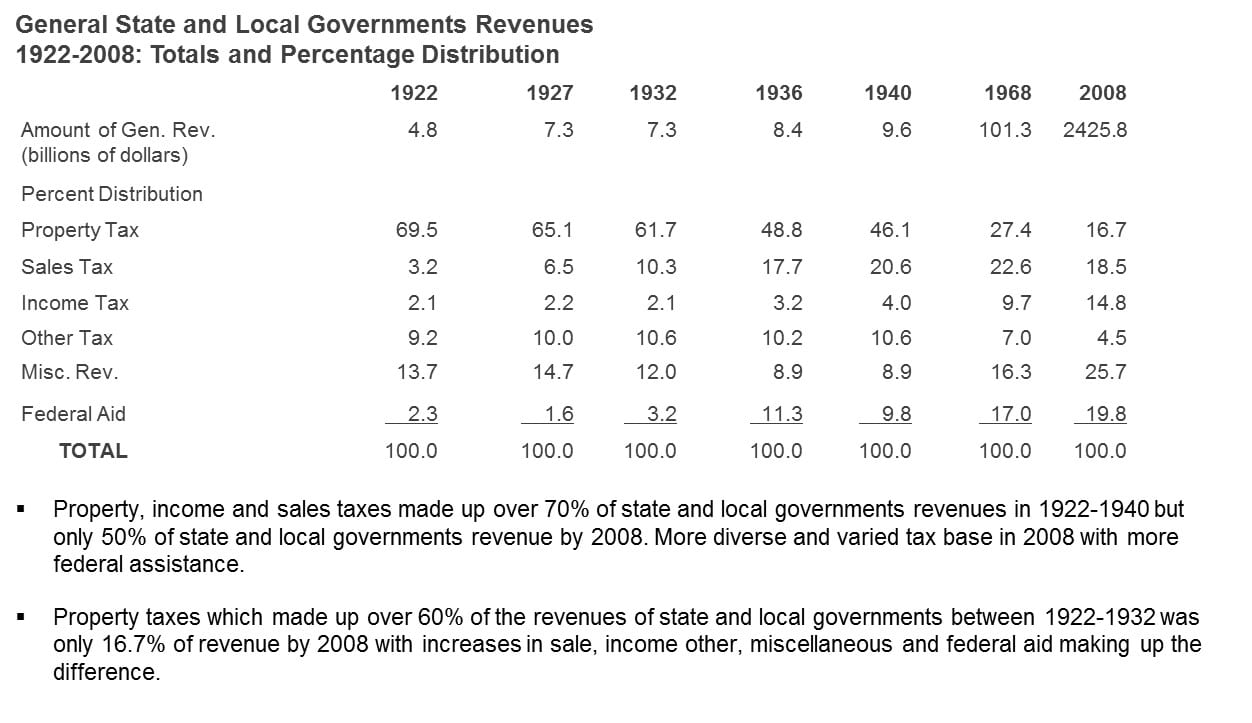

Diversification of Tax Sources to Prevent Over-Concentration of Source of Funding:

- Since the Depression of the 1930’s, state and local governments have diversified the source of tax revenues to reduce reliance on property taxes and to spread the burdens and reduce the risk of concentration. That diversity of tax sources has made a real difference in the eleven economic downturns since 1949, especially in 2008.

Use of debt limitation and tax limitation:

- Virtually all states impose some sort of limitation on the amount of debt or tax limitations or both.

- Municipal debt limits range from a percentage of a valuation of assessed property to a monetary amount.

- States handle debt for essential services differently than for non-essential.

- There have been recent attempts in some states to tighten local debt limits while others strengthen protections.

- Generally revenue bonds paid from the revenues of a municipal enterprise (water, sewer, bridge, tollway, electric system) are exempt from debt limits. So also are tax increment financing and appropriation bonds.

Refunding bonds are permitted in all states

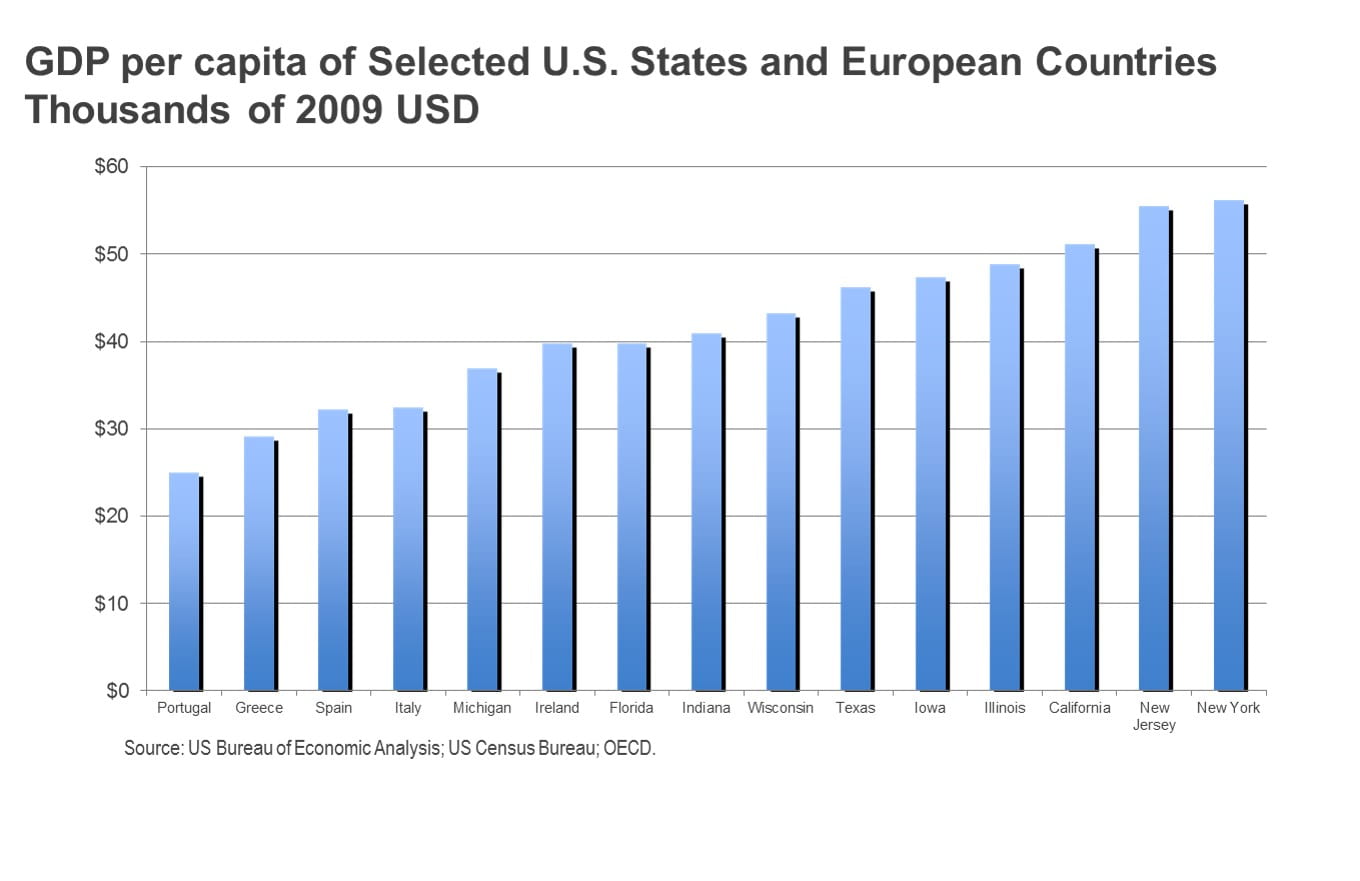

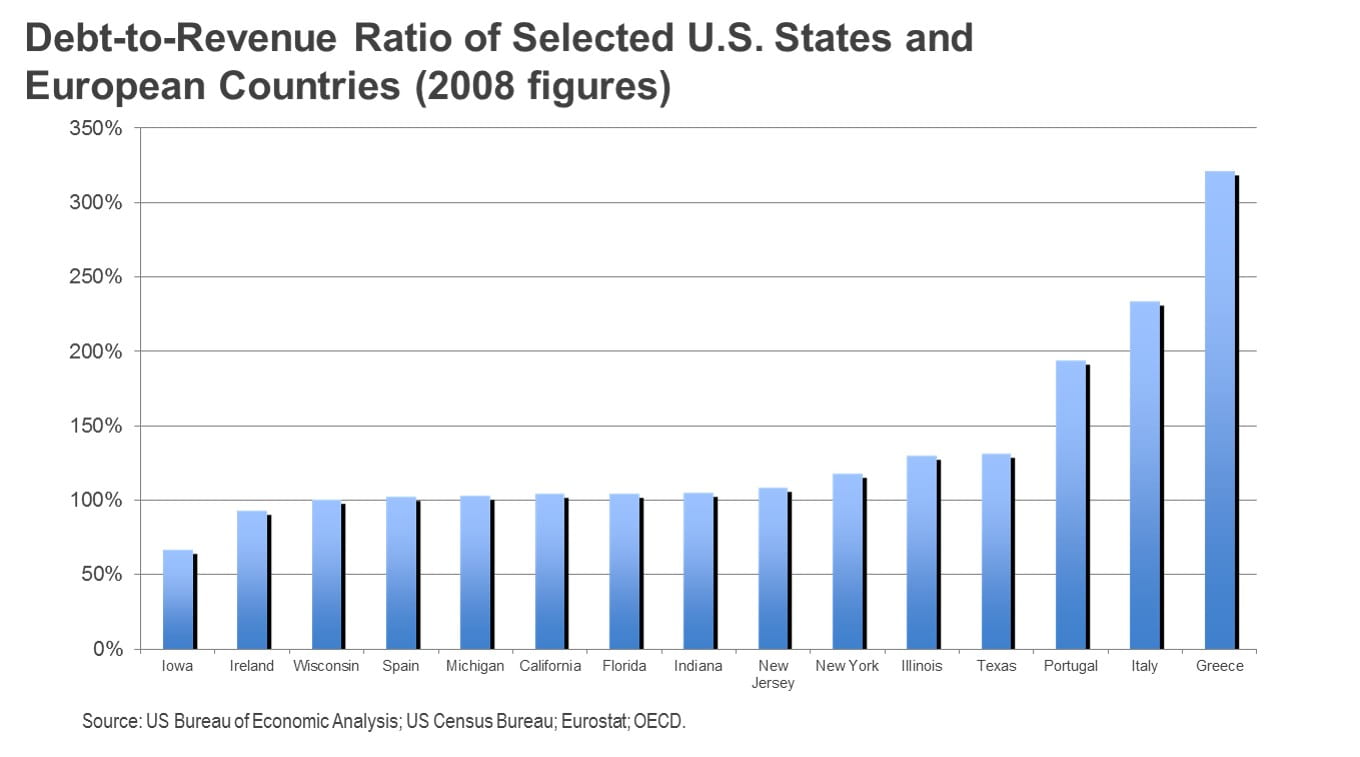

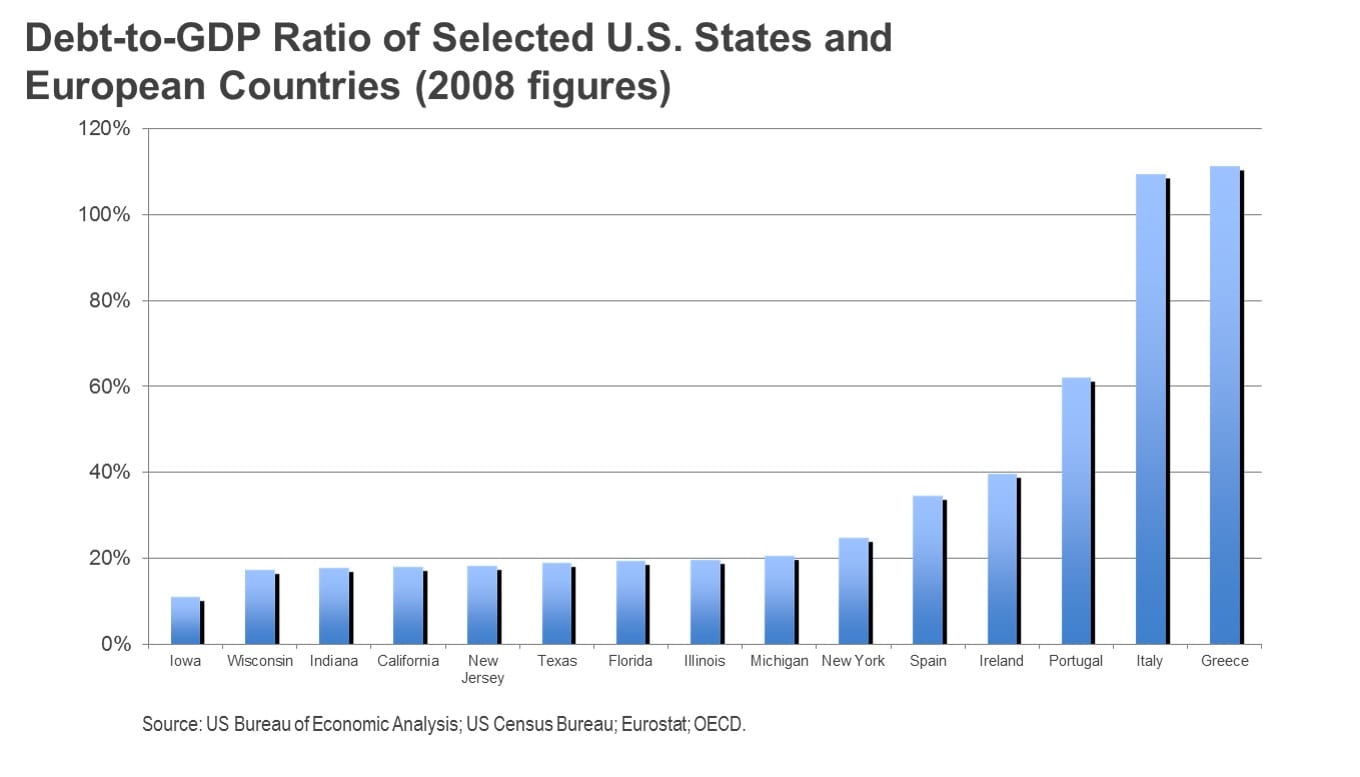

Our states and municipalities enjoy favorable GDP per capita, debt to GDP, and debt to revenue ratios compared to other sovereigns on a global basis:

- The per capita GDP of each of California, Texas, Florida, New York, Illinois and New Jersey (certain “Major U.S. States”) is higher than Portugal, Greece, Italy and Spain.

- The percentage of debt to revenue ratio is lower for Major U.S. States than Portugal, Italy and Greece.

- The percentage of debt to GDP is lower for certain Major U.S. States than Spain, Ireland, Portugal, Greece and Italy.

- The most recent example of our states enjoying a favorable GDP and Debt to GDP and Debt to Revenue Ratios compared to other Sovereigns on a global basis is China.

- China has:

- 31 provinces and regional governments.

- 391 cities.

- 2,778 counties.

- 33,000 townships.

- The combined debt of these local governments is approximately $3 trillion or 36% of China’s GDP (2012) (China National Audit Office). In 2015, China’s debt to GDP was approaching 40% from about 20% in 2007.

- 99 cities, 195 counties and 3,465 townships in China had direct debt 2013 exceeding 100% of their respective annual economic output (GDP).

- Interestingly, the central government in China is stepping up to help “refinance” the local government debt purchasing (exchanging) local debt by the central bank thereby lowering by 3-4% annually the borrowing cost from 500 basis points plus over treasuries.

- The USA has:

- 50 states.

- 3,031 counties.

- 19,522 municipalities.

- 16,364 townships.

- 37,203 special districts.

- 12,884 independent school districts.

- The combined debt of state and local governments is approximately $3 trillion (Federal Reserve Bank of St. Louis 2013) or 18.52% of the USA’s GDP.

- The highest debt to GDP for any state and its local government is approximately 26% for New York with the lowest being Wyoming at 5.25%. The percentage of debt to local GDP for large city issuers in the USA is generally less than 20% and in most instances less than 10%.

- China has:

Earlier articles in this series:

Earlier articles in this series:

Fiscal Distress Myths and Realities Part I: Default Rate

Fiscal Distress Myths and Realities Part II: Use of Chapter 9

Fiscal Distress Myths and Realities Part III: Consequences of Default

Fiscal Distress Myths and Realities Part IV: Can a Municipality File Chapter 9?

Look out for more parts of James Spiotto’s Fiscal Distress Myths & Realities coming soon.

James E. Spiotto, Co-Publisher © James E. Spiotto. All rights reserved