By James Spiotto

A. Types of municipality debt obligations in Chapter 9:

There are various types of voluntary municipal debt ranging from bond debt sold to the investing public, debt owed to vendors for goods and services in operation of the municipality to cost of workers and pension and health care benefits. In addition, municipalities can be subject to involuntary debt such lawsuits and claims for violation of civil rights, breach of contract, anti-trust violations discrimination, lack of due process and violation of constitutional rights (generally arising out of zoning and hiring and contracting), regulatory fines and penalties of state or federal government agencies.

- General municipal debt consists of:

- Bond or note indebtedness sold to the investing public, banks and financial institutions that consists of:

- General obligation bonds backed by the full faith and credit of the municipality and may also have a contractual or statutory pledge of revenue.

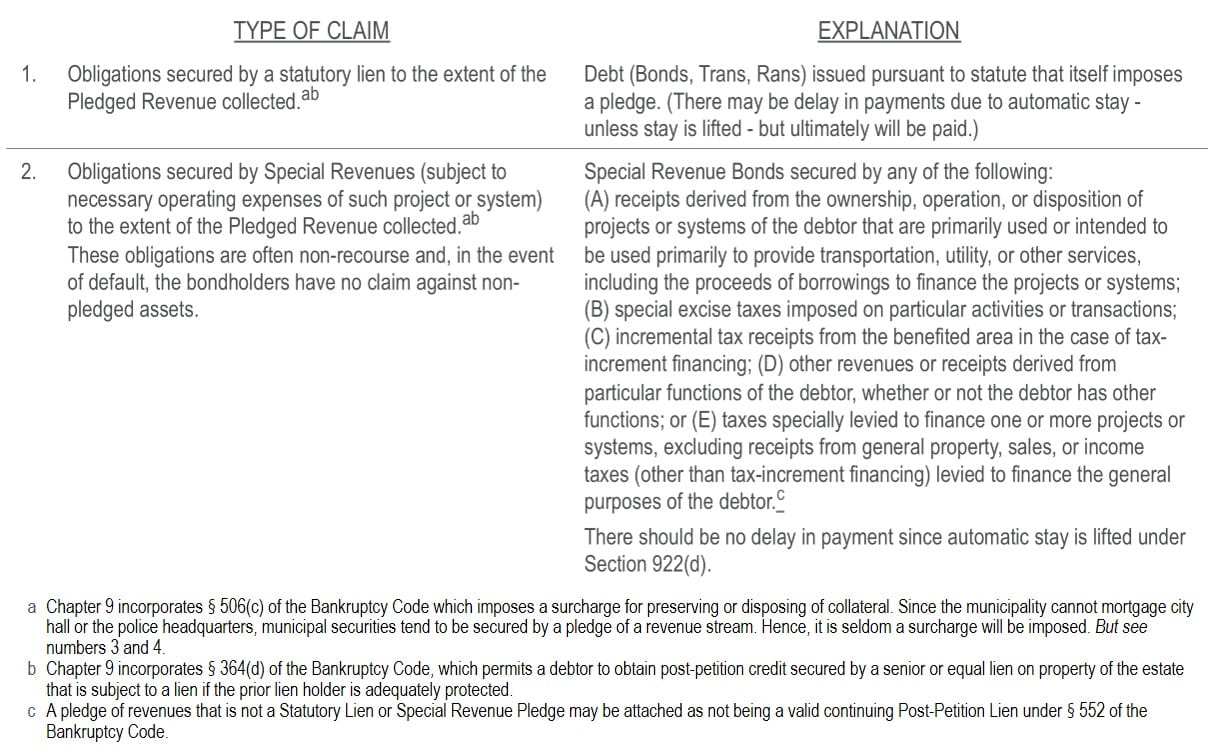

- Revenue bonds are generally only payable from the pledged revenue. Specific tax source or revenue related to the municipal enterprise financed and no other recourse to the issuing municipality. Generally, revenues from a municipal enterprise (such as water, sewer, electrical system) or from a specific dedicated tax source that is not to be used for any other purpose. These pledged revenues are referred to as “special revenues.”

- Municipal lease or appropriation backed bonds (non-recourse to municipality’s full faith and credit but recourse to annual appropriation or leased property. Note: cannot legally bind successor legislature to appropriate funds).

- Conduit financing which is non-recourse to municipality, must be for a general public purpose and the credit support is the non-profit or corporate entity benefited.

- Voluntary unsecured debt of vendors to the city for goods or services provided by the vendor. This is generally trade debt.

- Obligations for accrued by unpaid wages, employee benefits, health care, pension and other post-employment benefits (“OPEB”).

- Involuntary debt such as lawsuit judgments regulatory fines and penalties.

Municipality debt may be secured by special revenues as noted below or by a statutory lien on specific dedicated revenues that arise solely from a state statute and not by some additional action or agreement of the municipality. Under section 552 of the Federal Bankruptcy Code a contractual pledge by a municipality of revenues or property that is not subject to special revenues or statutory lien does not survive filing of Chapter 9 municipal bankruptcy and is not enforceable. Some state statutes and state constitutions provide that bonds may be subject to priority of payment, set aside of revenues as they are collected toward payment of the bonds or notes or mandatory appropriation of funds when payment is due of a municipality for the payment of bonds or notes. Generally, such priorities, set asides and mandatory appropriation provide that such tax revenues cannot be used for any other purpose until the bonds are paid. The municipality is subject to state statutory and constitutional provisions and should honor those provisions for priority, set asides or mandatory appropriation of payment in a Chapter 9 and after confirmation of a Chapter 9 plan of debt adjustment in order to be in compliance with state laws.

B. Summary of Chapter 9 priorities:

C. How are bonds and notes treated in Chapter 9?

| TYPE OF BONDS/NOTES | BANKRUPTCY EFFECTS |

| General Obligation Bonds | Post-petition, a court may treat general obligation bonds without a statutory lien as unsecured debt and order a restructuring of the bonds. Payment on the bonds during the bankruptcy proceeding likely will cease. Pre-petition, general obligation bonds are backed by the unlimited taxing power of the municipality (its “full faith and credit”) and are historically subject to conditions such as voter authorization, limitations on particular purposes, or debt limitation to a percentage of assessed valuation on the power of municipal entities to incur such debts. |

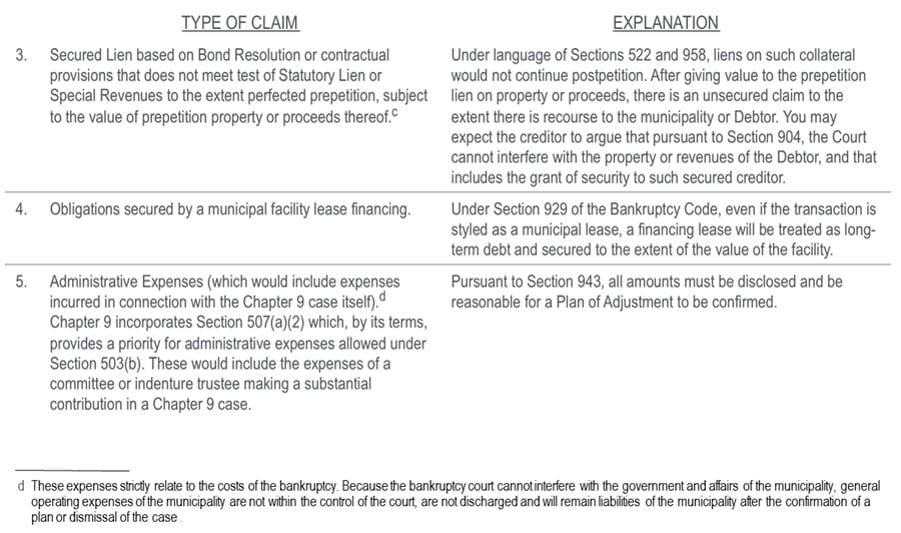

| General Obligation Bonds plus Pledged Revenues | Assuming that the general obligation pledge is an actual pledge of revenue and to the extent that it may be classified as a Statutory Lien or Special Revenues, this secured issuance will be respected and unimpaired and paid during a Chapter 9 to the degree it is consistent and authorized under state law. A Pledge of Revenues that is not a Statutory Lien or Special Revenues may be attacked as not being a valid continuing Post-Petition Lien under Section 552 of the Bankruptcy Code. This position may be questioned under Section 904 of the Bankruptcy Code given the prohibition that the Court not interfere with the Government Affairs or Revenues of the Municipality. |

| Special Revenue Bonds | A pledge on special revenue bonds will survive a bankruptcy filing.Pre-petition, a special revenue bond is an obligation to repay solely and only from revenues of a municipal enterprise (net of necessary operating costs in the case of a gross revenue pledge) that are pledged to bondholders. Special revenues are intended to be unimpaired and to be paid timely during a Chapter 9. The contemplated remedy for default often focuses on a covenant to charge rates sufficient to amortize the debt. Defaulted bondholders are expected to seek mandamus in court to require the municipal borrower to raise its rates. |

| Revenues subject to Statutory Lien | Assuming the pledge is authorized under state law through a statutory lien, the Bankruptcy Court should respect that statutory lien. Thus, as long as the revenues are subject to a statutory lien, payments to the bondholders should be protected post-petition. |

Chapter 9 – Legal Impact on Trustees and Bondholders of Municipal Debt

| • Special Revenue Bonds | • A pledge on special revenue bonds will survive a bankruptcy filing. |

| • Revenues Subject to Statutory Lien |

• Assuming the pledge is authorized and created by state law (statutory lien), the bankruptcy court should respect that statutory lien. Thus, as long as the revenues are subject to a statutory lien, payments to the bondholders should be protected. |

| •General Obligation Bonds | • Post-petition, a court may treat general obligation bonds without a pledge of a statutory lien or special revenues as unsecured debt and order a restructuring of the bonds. Payment on the bonds during the bankruptcy proceeding likely will cease. |

| • General Obligation Bonds Plus Pledged Revenues | • Assuming that the general obligation pledge is an actual pledge of revenue and to the extent that it may be classified as a statutory lien or special revenues, this secured lien on the tax revenues will continue to the extent taxes are collected. |

| • A contractual pledge of tax revenue provided for by the bond document that is not a statutory lien or special revenue will have any tax revenue collected before filing paid to the bondholders but after filing that lien is terminated. |

General Analysis of Chapter 9

How have general obligation bonds been treated in recent Chapter 9?

| Bankruptcy | Treatment |

| Sierra King Health Care District | The unlimited ad valorem tax G.O. Bonds were paid in full and recognized as having a statutory lien and being secured by special revenues. |

| Jefferson County | G.O. Warrants were basically paid in full and no objection by Holders but there were some delayed payments. |

| Detroit | Revised proposed treatment in plan of adjustment pursuant to settlement whereby the LTGOs have a 34% recovery and impaired but settlement with ULTGOs as secured 74% recovery for insurers – Bondholders to be paid 100% but insurers to make-up the differences between 74% and 100% and Distributable State Aid G.O.s treated as fully secured and unimpaired with 100% recovery. |

Note: Section 552 of the Bankruptcy Code has been interpreted to date to terminate a contractual pledge or promise to pay future tax revenues to be levied and collected after filing may be limited to pre-petition tax revenues levies and not revenues levied and collected from levies after the petition date. Any attempt of a municipality to deprive a general obligation bond of tax payments created and that come into existence solely by (a) means of a state statute (“Statutory Lien”) or (b) that are constitutional or statutory mandated priority, set aside, or appropriation or (c) means that qualifies as Special Revenues will create a confirmation objection of failing to comply with state law.

James E. Spiotto, Co-Publisher © James E. Spiotto. All rights reserved (2015).